US 2024 presidential election: The potential global impact

- 19 September 2024 (15 min read)

A tight race

Before the summer we reviewed the upcoming presidential election and its likely impact on the US economy1 . At that time, President Joe Biden had just bowed out of the race and been replaced by Vice President Kamala Harris. Former President Donald Trump initially led Harris by a modest amount in overall polling approvals, though by less than he had led Biden. Since then, Harris has seen an improvement in ratings. Rising from a deficit of 1.7 points, she now leads Trump by 2 points2 .

Exhibit 1 illustrates this polling boost has spilled to marginal states. Harris has significantly reduced Trump’s lead in all marginals: all now appear competitive, with Harris leading narrowly in Nevada, Michigan and Wisconsin, and far ahead in New Hampshire. Only Florida remains staunchly pro-Trump.

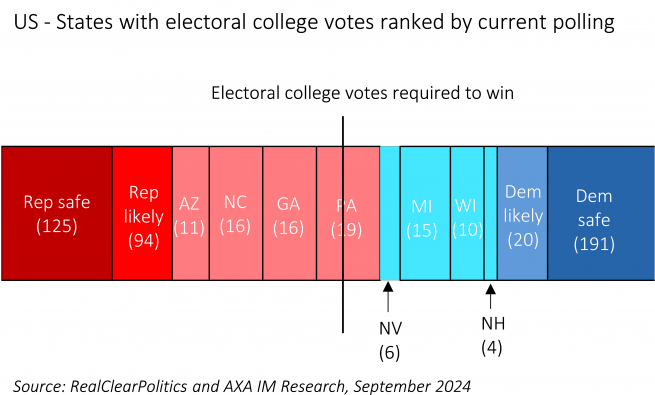

Exhibit 2, however, shows that based on this polling, Trump still wins the electoral college count, although we would argue that 7 of 8 key states are now within polling error margins. Allan Lichtman, the US historian who has correctly predicted each election since 1984, recently announced his prediction for a Harris win after Teddy Kennedy Junior’s withdrawal.

Exhibit 3 suggests the election is far from decided. Eight years ago, Hillary Clinton enjoyed far larger leads than Harris has over Trump but went on to lose. Four years ago, Biden also had a much bigger poll lead, but eventually only won with half the lead predicted and by 43k votes in three key states. Harris’ convincing performance in September’s televised debate has arrested a tentative softening in her lead after the initial honeymoon and post-Democrat Convention support.

- PGEgaHJlZj0iaHR0cHM6Ly93d3cuYXhhLWltLmNvbS9pbnZlc3RtZW50LWluc3RpdHV0ZS9tYWNyb2Vjb25vbWljcy91cy0yMDI0LXByZXNpZGVudGlhbC1lbGVjdGlvbi1wcmV2aWV3LXRydW1wLWZhY2VzLW5ldy1hZHZlcnNhcnkiPlBhZ2UgRC4g4oCcVVMgMjAyNCBwcmVzaWRlbnRpYWwgZWxlY3Rpb24gcHJldmlldzogVHJ1bXAgZmFjZXMgbmV3IGFkdmVyc2FyeSZxdW90OyAgQVhBIElNIFJlc2VhcmNoLCAyNiBKdWx5IDIwMjQ8L2E+LiA=

- UmVhbCBDbGVhciBQb2xpdGljcywgMjIgQXVndXN0IDIwMjQg

In this paper we consider the impact the US election could have globally. We believe a Harris win could have a material impact on the outlook for domestic activity – particularly distributionally – albeit our expectation remains she would face a split Congress, which would hamstring bolder policy. Her victory’s impact on the world would thus likely be limited to the not inconsequential spillover effects from US growth.

Yet a win for Trump would have more direct impacts for many economies and could start a chain of events that could lead to many indirect effects. In particular, we consider the impact of Trump’s proposed tariff policy. While we have explained that in price terms this is something we would expect to be felt more by US consumers than foreign producers, in volume terms this is likely to have a material impact on China – the focus of Trump’s campaign ire – with a proposed 60% tariff. By contrast, while the Eurozone would face a plausibly smaller 10% tariff – from the roughly 5% weighted tariff currently – trade tensions could rise further in the face of any European Union (EU) retaliation or from the EU’s separate efforts to address carbon emissions through its Carbon Border Adjustment Mechanism.

These policies are likely to drive US interest rates and the dollar higher – despite Trump’s protestations to the contrary. This would impact the global economy, particularly emerging markets.

We also consider the implications of Trump’s statements on security. His antipathy to North Atlantic Treaty Organization (NATO) and suggestion of a settlement in Ukraine could signal a period of security withdrawal from Europe. In the face of persistent Russian aggression, Europe could have to revert defence spending to levels that prevailed before the post-Soviet Union ‘peace dividend’ – which is something few European economies are well placed to fund. In Asia, Trump has also threatened less security provision, or a moretransactional relationship. This could also see a reduction in US security presence here, with implications for many nations in Southeast Asia.

More broadly, we examine Trump’s likely environmental stand. Reneging on the Paris Agreement in his first term, we expect Trump to weaken climate change avoidance policies. While we have argued that Trump is unlikely to reverse Biden’s signature spending bills3 completely, he is likely to oversee deregulation of oil and gas production, boosting output for both. In the short term this is likely to lower energy costs, softening inflation outlooks globally. However, over the medium to long term this is likely to keep US greenhouse gas emissions high.

We consider the possible impact on Europe and China, before broadening our outlook to consider Emerging Asia, Japan, Mexico, Canada and Emerging Europe.

- PGEgaHJlZj0iaHR0cHM6Ly93d3cuYXhhLWltLmNvbS9pbnZlc3RtZW50LWluc3RpdHV0ZS9tYWNyb2Vjb25vbWljcy9tYWNyb2Vjb25vbWljLXJlc2VhcmNoL3dpbGwtdXMtcHJlc2lkZW50aWFsLWVsZWN0aW9uLWVuZGFuZ2VyLWludmVzdG1lbnQtYm9vbSI+UGFnZSBELiDigJxXaWxsIHRoZSBVUyBwcmVzaWRlbnRpYWwgZWxlY3Rpb24gZW5kYW5nZXIgYW4gaW52ZXN0bWVudCBib29tP+KAnSBBWEEgSU0gUmVzZWFyY2gsIDI3IE1heSAyMDI0PC9hPi4g

Disclaimer

This website is published by AXA Investment Managers Asia (Singapore) Ltd. (Registration No. 199001714W) for general circulation and informational purposes only. It does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities. It has been prepared without taking into account the specific personal circumstances, investment objectives, financial situation or particular needs of any particular person and may be subject to change without notice. Please consult your financial or other professional advisers before making any investment decision.

Due to its simplification, this publication is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this publication is provided based on our state of knowledge at the time of creation of this publication. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

All investment involves risk, including the loss of capital. The value of investments and the income from them can fluctuate and investors may not get back the amount originally invested. Past performance is not necessarily indicative of future performance.

Some of the Services and/or products may not be available for offer to retail investors.

This publication has not been reviewed by the Monetary Authority of Singapore.