CIO Views: Investors must adapt to changing fundamentals

- 03 April 2025 (5 min read)

KEY POINTS

Chris Iggo, CIO AXA IM Core

Fresh market disruption

Investors face both growth and inflation risks. Uncertainty around policymaking and shifting global political and economic relations have pushed up market volatility and investors are struggling to adapt portfolios to changing fundamentals. So far, it appears growth risks dominate. This is most obvious in the downward revisions to US GDP forecasts, S&P 500 earnings expectations and the relative performance of US versus European markets. For the last decade, the US equity market has had an earnings growth premium over other markets - justifying the valuation premium that has increased since the pandemic. While the US market’s long-term strengths are not in doubt, some of them are challenged in the near term by concerns over the impact of trade and domestic policies on confidence and spending.

Meanwhile, inflation risk premiums and bond yields are stable. Tariffs will disrupt consumer prices, but the bigger delta is on growth expectations. This suggests that US equity market underperformance might persist. Bonds have outperformed and we still retain a positive view towards credit, but for the bond-equity valuations adjustment to go much further, current rate expectations need to be validated. If investors and market valuations keep marking down growth prospects however, a dovish Federal Reserve pivot becomes more likely. If stocks move further away from extreme overvaluation, 10-year US bond yields could eventually move below 4%, extending the surprising relative moves seen already this year.

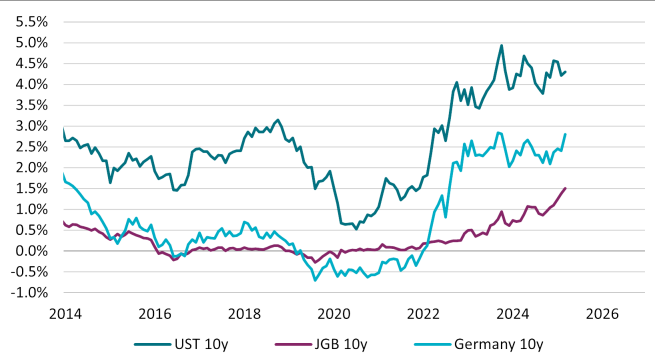

Alessandro Tentori, CIO Europe

Bunds: Losing my religion

German government bonds (Bunds) suffered their worst day in Eurozone history on 5 March, when the yield on the 10-year benchmark Bund increased by 30 basis points and the iBoxx Germany Sovereign index declined by a notable 1.8%. The move was uniformly spread across all European government bond curves, with little volatility on cross-country spreads, while the iBoxx Eurozone Sovereign index declined in line with Germany.

The reason for such unusual volatility was Germany’s perceived drift away from fiscal prudence. In fact, Germany has only adopted a countercyclical expansionary fiscal stance on two occasions since 1999, thus cumulating a modest 14% in budget deficit since the 2008 global financial crisis. By comparison, France has cumulated almost 80% and Italy almost 70% in budget deficits over the same period.

In our view, the sharp market reaction is linked to Berlin moving away from championing orthodox fiscal policy to deploying the ample fiscal space at its disposal for structural projects. While this may signal an epochal transition in Europe’s economic framework, the message for markets is straightforward. It means more Bunds will have to be issued to finance German structural projects; German GDP growth will be boosted in the medium term; and other Eurozone countries might adopt a similar fiscal approach. This is good news for advocates of structurally high(er) yield levels.

Ecaterina Bigos, CIO Asia ex-Japan

A tale of two economies

Both India and China are at turning points in their respective economic and policy cycles – and this has implications for asset valuations. Structurally and cyclically, both economies are going through a softer patch. While the Chinese government has introduced stimulus measures, India is keen to consolidate its fiscal position to improve macroeconomic stability. China currently has a high level of household savings - 34% at the end of 2024. And, structurally, it has a lower share of consumption to GDP, at 45% compared to India’s 60% (69% in the US). A rise in personal consumption to 60% of GDP would equate to annual consumption of some US$10trn on today's GDP; $3trn higher from the current level. Achieving this scale of retail support requires market reforms and concerted policy efforts, with incentives directed at consumers.

Conversely, India’s ambition to become a US$10trn economy with greater manufacturing share is dependent on a continued and accelerated infrastructure rollout to reach China’s standards. India accounts for only 3% of global manufacturing, half of where China stood in 2000. Its manufacturing is more dependent on other economies, operates lower down the value chain and incentives are still small in a global context. For now, its success is in exporting more services, which account for 55% of GDP, with manufacturing at 15% but largely stagnant for the past decade.

Asset Class Summary Views

Views expressed reflect CIO team expectations on asset class returns and risks. Traffic lights indicate expected return over a three-to-six-month period relative to long-term observed trends.

| Positive | Neutral | Negative |

|---|

CIO team opinions draw on AXA IM Macro Research and AXA IM investment team views and are not intended as asset allocation advice.

Rates | Timing of further rate cuts is uncertain, with no clear direction for bond yields | |

|---|---|---|

US Treasuries | Fed on hold; chance of lower yields if growth concerns persist | |

Euro – Core Govt. | Recent sell-off has improved valuations; ECB still expected to cut rates | |

Euro – Peripherals | Spreads stable but need to watch for any new spending plans | |

UK Gilts | Fiscal uncertainty and Bank of England on hold drive stable yields | |

JGBs | Yields can move higher with expectations of further monetary policy tightening | |

Inflation | US and UK inflation breakeven rates look too low |

Credit | Recent widening in spreads should maintain investor interest | |

|---|---|---|

USD Investment Grade | Yields attractive relative to Treasuries | |

Euro Investment Grade | Corporate spreads are expected to remain stable; tariffs are a risk | |

GBP Investment Grade | Risk of wider spreads if growth outlook remains weak | |

USD High Yield | Technical factors and valuations remain supportive, equity weakness a risk | |

Euro High Yield | Attractive yields and improved financing environment | |

EM Hard Currency | Need to monitor effects of tariffs on different countries |

Equities | Global rotation out of the US could persist on tariff uncertainty | |

|---|---|---|

US | Credible plan to resolve tariff uncertainty will allow business cycle to continue | |

Europe | German fiscal plan is boosting long-term growth expectations | |

UK | Attractive valuations, but policy needs to become more growth positive | |

Japan | Upturn in industrial cycle will benefit Japanese stocks; tariffs are a risk | |

China | Tech sector leading market recovery on AI developments; tariffs are a risk | |

Investment Themes* | AI-related spending continues to be strong |

*AXA Investment Managers has identified six themes, supported by megatrends, that companies are tapping into which we believe are best placed to navigate the evolving global economy: Technology & Automation, Connected Consumer, Ageing & Lifestyle, Social Prosperity, Energy Transition, Biodiversity.

Disclaimer

This website is published by AXA Investment Managers Asia (Singapore) Ltd. (Registration No. 199001714W) for general circulation and informational purposes only. It does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities. It has been prepared without taking into account the specific personal circumstances, investment objectives, financial situation or particular needs of any particular person and may be subject to change without notice. Please consult your financial or other professional advisers before making any investment decision.

Due to its simplification, this publication is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this publication is provided based on our state of knowledge at the time of creation of this publication. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

All investment involves risk, including the loss of capital. The value of investments and the income from them can fluctuate and investors may not get back the amount originally invested. Past performance is not necessarily indicative of future performance.

Some of the Services and/or products may not be available for offer to retail investors.

This publication has not been reviewed by the Monetary Authority of Singapore.